“If trouble comes when you least expect it, then maybe the thing to do is to always expect it.” – Cormac McCarthy, writer

ECONOMY: INFLATION REMAINS IN THE SPOTLIGHT

Those that have been lucky enough to live through the year 2000s tend to always expect the unexpected. It’s a matter of experience. Those that were financially borne post-Great Financial Crisis have a different mindset, shaped by years of bull markets and low interest rates. More than long-term crisis, the latter have experienced corrections, at times severe corrections, but always followed by sudden rebounds, often orchestrated by the FED put. In hindsight, even 2022 turned out to be a correction.

To be clear: we are neither advocating for an Armageddon-type scenario nor are we hoping for one. Why would we? But what keeps us up late at night, and if you are an habitue of our quarterly Outlooks you know we have had this feeling for some time, is that risky assets have lost their ability to price-in the concept of uncertainty, of which nowadays the world is (unfortunately) full of. Admittedly, any uncertainty becomes a certainty at one point, it reveals itself, unleashing the outcomes following its transformation. Such outcomes do not necessarily have to be hostile. But the more uncertainties you face, the higher the probability one or more of these turn out to be unfriendly.

At the time of writing, putting on a happy face, as the Joker used to say, is a daunting task. Global economies battling with slowing growth and high inflation, controversial elections in major developed countries, multiple geopolitical instabilities (this is a euphemism, I am trying to downplay the risk to avoid being dubbed a perma-pessimist, because the reality is we are facing two wars occurring simultaneously), real estate cracks, high equity valuations, … but all we look for is whether the Federal Reserve (FED) will cut rates, and by how much. (As if the FED could save everyone from everything.) We are so obsessed on what the next move will be, that we spend time scrutinizing the exact words that are being used in the minutes of the Federal Open Market Committee (FOMC) meeting, or during more general interviews, that we lose sight of the fact that they (i.e. the FOMC members) are humans too and do not have much more predictive power than we (i.e. investors) do. I believe by now we have had multiple proofs of their inability to forecast where the economy is heading to. Hence, one more reason to start pricing the fact that something may go wrong.

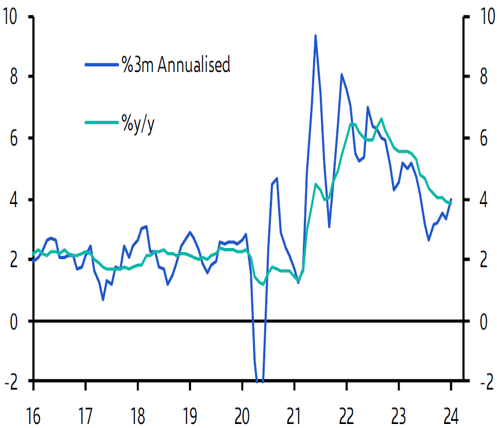

The US economy is indeed in a better shape than many of us were envisaging a year ago. The expectations that the FED would begin cutting rates as soon as this summer has had a positive effect on both businesses and consumers. On the one hand, it fuelled the improvement on a three-months basis of the purchasing manager indexes (PMIs – graph top-right of the page). Whether the surveyed data will be followed by actual capital expenditures will have to be proven over the remaining of the year. Similarly, also consumers seem to believe the economic outlook is bright, as retail sales have recently (once again) surprised to the upside. Yet, beneath the surface, some pieces of the puzzle are starting to detach from the bigger picture. Inflation is back on the rise (chart top-left on page 2), with multiple alternative measures of the gauge pointing to a resurgence in prices. Excess savings, one of the major contributors to the rise in consumption expenditure over the past few years, are quickly drying up and are expected to be drained by the summer. Thus, there is no surprise in witnessing that the credit card delinquency rates continue to grow, similarly to the number of Chapter 11 bankruptcy filings. Moreover, the job market cannot be considered as being overheated anymore, which is surely a good thing. However, the increased number of layoffs within temporary workers has usually been a bad omen for the economy; company first stop hiring, then begin to layoff temporary workers, and finish by cutting full-time employees, which usually coincides with the making of a recession.

The resilience of the US economy is remarkable. Driven by very flexible labour conditions, and by an exceptional propensity to spend, it has been able to withstand one of the steepest rises in interest rates over the last decades. If rates will in fact fall back over the upcoming months, then the risks to the economy will remain contained. On the other hand, if inflation forces the Federal Reserve to keep rates where they stand today, then we must assume the damages to the economy will be meaningful. As we write, the mortgage payment (principal and interest) as a percent of a median income has risen above 40% for first-time homebuyers, a level that we consider unsustainable, and which may shut down the housing market. Additionally, corporate America (and not only them), who has taken advantage of an era characterized by low interest rates and advantageous tax rates to achieve outstanding profit margins, and who has been wise enough to refinance its debt as the pandemic took over, will also face a day of reckoning should interest rates stay where they are for a longer period.

As a result, having in mind that this is an electoral year, which means both the FED and the incumbent government will do anything in their power to avoid a meaningful deterioration in either the economy or financial markets, we reiterate what we have outlined in past Market Outlooks; we remain doubtful that inflation will fall as fast as consensus is expecting, and thus we believe interest rates will remain elevated for longer than currently forecasted by many market participants, which leads us to expect some troubles ahead.

Outside of the United States, the environment presents a mixed picture. In Europe, including Switzerland, the economy continues to decelerate, which has prompted the Swiss National Bank (SNB) to cut interest rates. The SNB is officially the first central bank among developed nations to start the cutting cycle. Europe is expected to follow soon, as sluggish growth and quickly falling inflation will allow the European Central Bank to implement its first cut during the summer months. As of today, the ECB is expected to cut three times before the year end, which should help the economy avoid a severe recession.

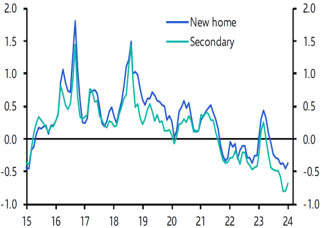

China has yet to recover from its real estate-driven hangover. The real estate sector still suffers from falling house prices and a deceleration in the sales of new homes (chart to the right). However, central authorities have begun implementing supportive measures; interest rates have been lowered, which has sent the mortgage rate for first-time buyers to a decade low, and the initial downpayment level has been scrapped to incentivize first-time buyers. Outside of the real estate market, conditions have improved slightly as well. Tourism numbers are at the highest since pre-pandemic levels, and the country’s exports, despite Europe’s shaky trend, have been grinding higher, thanks to a weakening currency and lower prices. Lower prices however are a double-edge sword, as the country has been battling against disinflationary trends since the beginning of ’23. Still, while not out of the woods yet, there is a glimmer of hope.

FIXED INCOME: STICKING TO QUALITY

Consistent with our economic outlook, we echo our past preference towards the safer segment of the asset class. Government bonds and high-quality investment grade issuers remain in our view the most attractive risk-adjusted investments in the fixed income space.

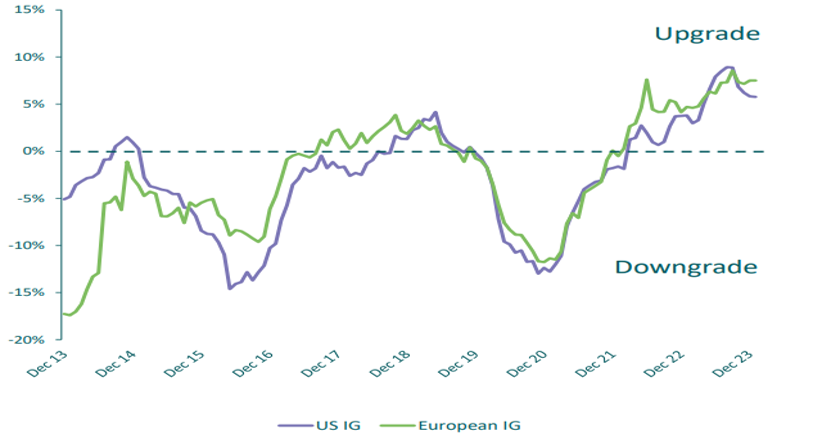

The recent move higher in global rates will put further pressure on highly indebted companies (for the moment, we want to give governments the benefit of the doubt), hence the ability to sustain higher debt-servicing costs becomes paramount in the current environment. For this reason, we continue to view as attractive companies with low leverage and elevated cash-to-debt multiples, both of which the investment grade space is plentiful of. With such characteristics, one would think that the price to be paid for owning such instruments is higher than lower quality names; on the contrary, while valuations did rise over the past months, these companies are still trading at levels that are only slightly more expensive than the long-term average. More surprisingly, investment grade names are much cheaper when compared to the high yield segment of the market, which is inconsistent with the deteriorating balance sheets and the rise in the default rate of the businesses in this field. This dichotomy is underscored by the rating drift (the number of rating upgrades against that of rating downgrades), which has been positive for the investment grade sector for both 2023 and 2024 (chart top-left), while clearly negative for high yield names during the same period.

Valuations are the main reason for our downgrade of emerging market debt, alongside the risk that a stronger USD poses to the refinancing capabilities of emerging market issuers. On the other hand, the healthy balance sheets of European banks, emphasized by very high capital ratios, and credit spreads that hover close to the long-term averages, make subordinated debt of high-quality issuers attractive.

One final word on duration. We do not and cannot rule out the possibility that interest rates move higher from current levels, especially if inflation remains elevated and gives the FED further headaches. However, we do believe that over the medium-term, the current yields represent an attractive investment opportunity, thus we would not regard as absurd an increase in portfolio duration towards the market benchmark.

![]()

The resilience of the US economy is remarkable (…) yet if inflation forces the FED to keep rates elevated (…) the damages to the economy will be meaningful.

![]()

EQUITY: EARNINGS GROWTH EAGERLY AWAITED

If you read until this point, you may guess what is waiting for you. To make a long story short, if you look for companies that have the potential for earnings growth, you overpay, with the risk of achieving a very poor return over the medium to long- term. On the other hand, if you wish to buy stocks that are cheap, you may end up in what is referred to as value traps, i.e. stocks that look undervalued but that are undervalued for a reason. In this case, businesses whose earnings growth potentials are very limited. Evidently, we are painting everyone with the same brush, and this is incorrect. But it does give you an idea of what the US equity market looks like presently.

In the meantime, the Magnificent 7 became the Magnificent 5, as Tesla and Apple have failed to live up to (high) expectations. If you recall, we have mentioned in the past that successful companies, no matter how resilient their business is, will suffer from a normalization in earnings growth and profitability. This is exactly what is happening, and more of the same should be expected going forward. Conversely, the last earning season (Q4/’23) has shown an improvement in the breadth of companies with positive earnings growth, although the overall picture is still unsettling as the earnings growth of the S&P 494 stood at -10.5%. Expectations for the first quarter of this year are not much different, with the earnings of a handful of companies expected to grow at roughly 80%, while the rest of the market is settling for a more modest 3%. Unexciting.

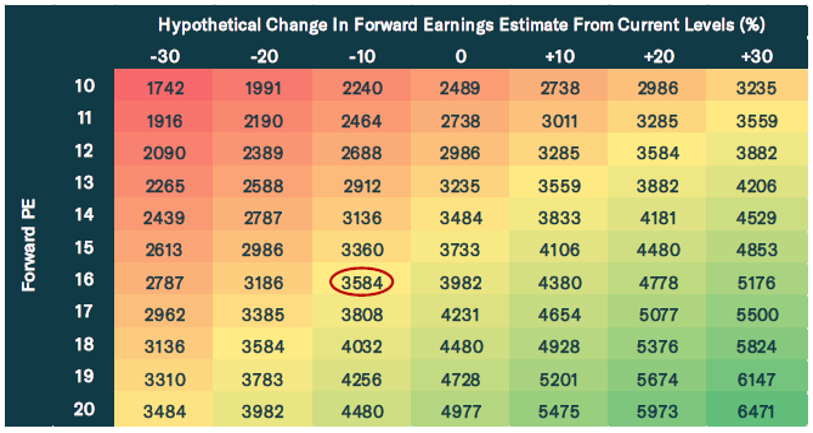

The strong returns experienced in equity markets over the past semester are to be attributed to mere multiple expansion. Now, earnings growth must follow; to justify current valuations, the former must rise by 10% over the next 12 months. This is also what the consensus expects. Given all we have written until now, it should be no surprise to read that we believe the road to a 10% growth rate in earnings is full of traps. On the other hand,should we fall into a recession, which would bring along a normalization in the valuation multiple and a fall in earnings of roughly 10%, the fair value of the market is estimated to be at roughly 3’600 (see table at bottom-left). Therefore, at today’s valuations, we would avoid chasing the current rally.

Year-to-date, European equities have staged a remarkable performance, defeating both the S&P 500 and the Nasdaq. How is this possible? To start with, the financial sector has benefited from rising interest rates (3 of the top 5 performers in Europe are banks), and the sector exposure within European indexes is heavier compared to the US. Secondly, the valuation of the entire region is fair (not expensive), which helped contain the recent losses following another spike in interest rates. Speaking of valuations, the European market has never been so cheap compared to the US market. Does this represent a buying opportunity or a value trap? It’s difficult to tell. If China’s economic momentum resumes, and Germany fixes the productivity issues it has suffered from for several years, European companies may be trading at bargain prices. Otherwise, one needs to do more cherry-picking to ensure avoiding unpleasant surprises.

The SNB cut has prompted investors believe we stand in front of a prolonged period of Swiss Franc (CHF) weakness, which may be very advantageous for most Swiss companies, worldwide exporters by nature. If we take the CHF out of the equation, as it is tricky to assume its long-term weakness considering the deficits of the US federal government and the highly- indebted European nations, investors should still find the Swiss equity market attractive, as it offers the opportunity to purchase high quality businesses with high profitability, at decent valuations, especially in the mid-cap segment.

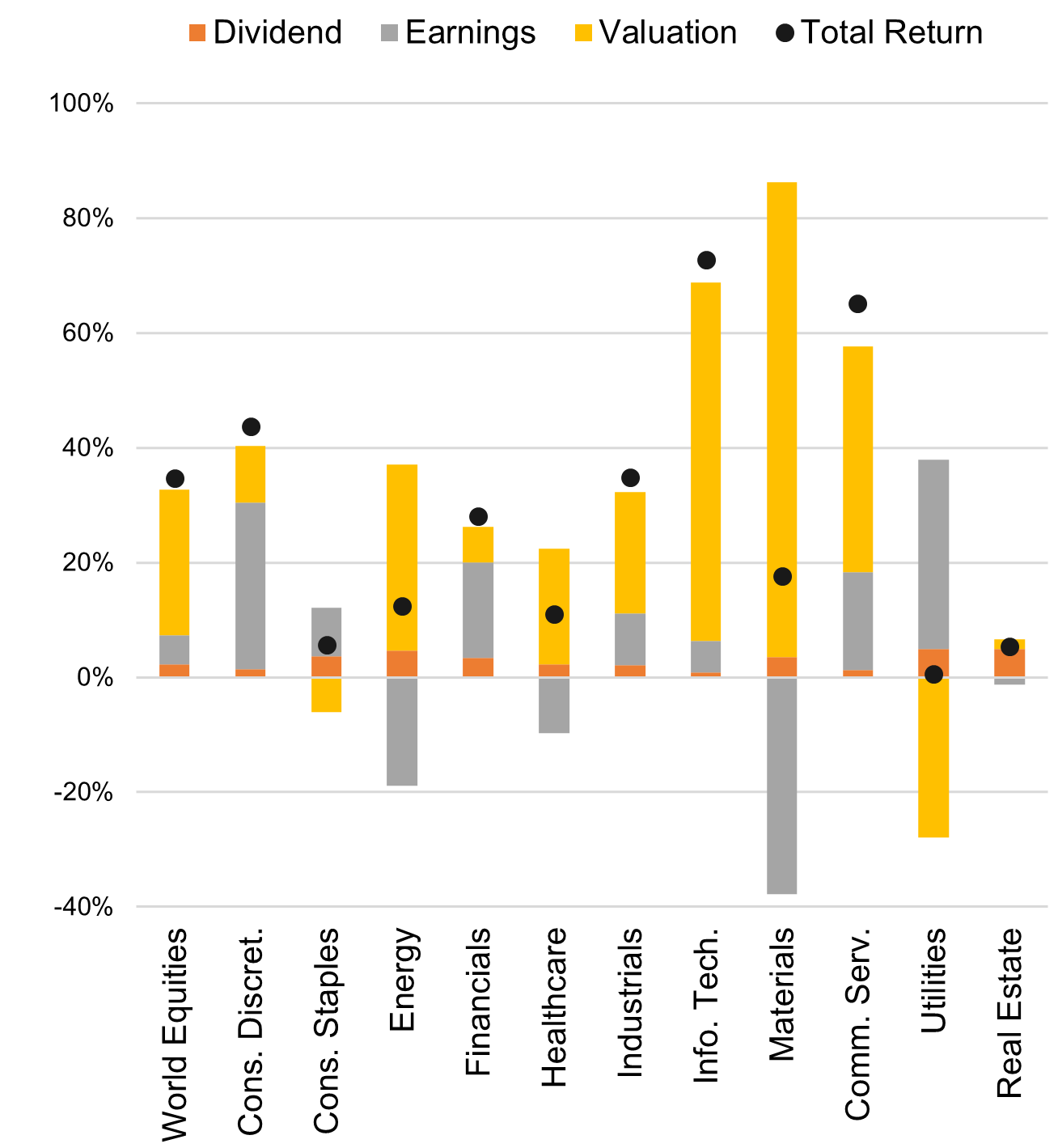

A few and final words regarding sectors performance and preferences. To date, the standout performers have been Communication Services, Energy, and Information Technology. Not surprisingly, given the rise in oil prices, and the returns shown by Nvidia, Netflix, Meta, and the likes. While we believe Communication Services and Information Technology will remain the predominant source of growth in the upcoming years, we also think that expensive valuations make these two sectors less attractive than their growth profile would otherwise imply. Given our conservative stance and taking into account the growth prospects of the underlying constituents, we still consider the energy sector and the healthcare sector as more attractive in the short term.

CURRENCIES AND COMMODITIES: FUNDAMENTALS NEGLECTED

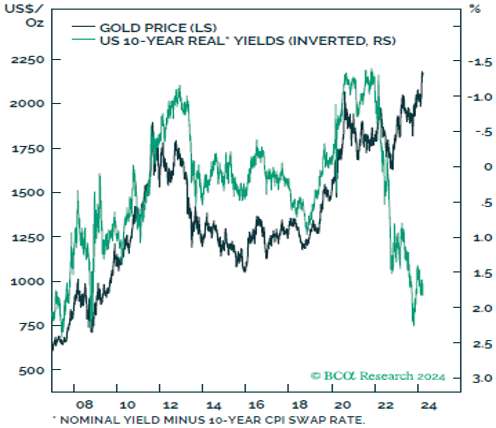

As outlined during previous Market Outlooks, we see the underinvestment by the mining sector as a reason to be bullish towards industrial metals in the long term. Inventories of specific metals, such as copper and zinc, are close to a decade low, and China’s timid signs of recovery add to the positive scenario. Shorter-term though, if we are correct in forecasting a risk-off phase, we believe the market will offer better entry points. A similar picture, although for different reasons, applies to gold. In 2023, while real interest rates were on the rise, the yellow metal has remained remarkably resilient (chart to the right), and produced an outstanding performance year-to-date, on the back of the escalating conflict in the Middle East and, in our humble opinion, the formation of some cracks in the trust investors place in central bankers. It’s difficult to assign a fair value to gold, but looking at its exponential move, while remaining bullish towards the metal, we believe a setback would only be natural (and welcomed).

The conflict in the Middle East remains at the heart of the latest rise in oil prices. OPEC+ decision to extend production cuts until mid of this year has added further propellent to the move (please excuse my wordplay). Over the short-term, oil and oil companies remain one of the best hedges against any escalation in the Region.

The US dollar (USD) has been appreciating against all major currencies, recouping most of the losses experienced following last year’s alleged FED’s pivot. The momentum is in its favor, and the yield spread differential will support the greenback until a monetary policy surprise kicks in. Longer-term valuations point in the opposite direction, with the USD bound to depreciate.

Speaking of valuations, the Japanese Yen looks extremely undervalued, and in an environment where a risk-off mood prevails, it is highly likely that the Japanese currency will appreciate substantially. It thus could be used as a portfolio hedge, in case of need.1

About the author

LFG+ZEST SA