“Breaking up is like knocking over a coke machine. You can’t do it in one push, you got to rock it back and forth a few times, and then it goes over” – J. Seinfeld.

We don’t know how much the comedian Jerry Seinfeld knows about macroeconomics and the makings of recessions, but the phrase he pronounced in a 1997 episode of the sitcom Seinfeld very well describes the current global macroeconomic picture. High inflation (and high interest rates) are the invisible arms that press against the coke machine, trying to knock it over. The US consumer is what keeps, for the moment, the coke machine standing on its feet – gravity. But gravity, once the coke machine rolls over, can be a double-edge sword.

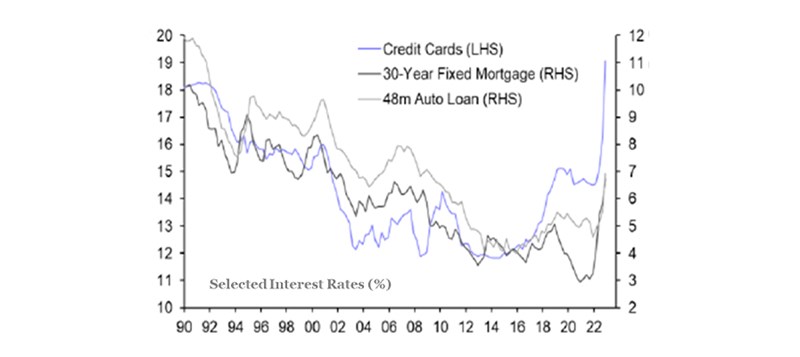

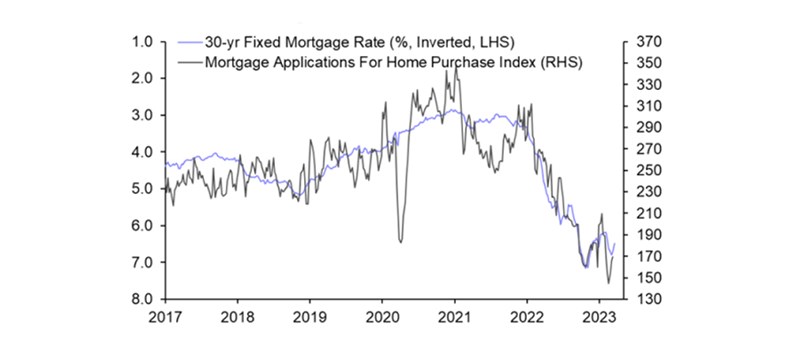

Our view is that a recession is no longer a matter of if, rather a matter of when. Leading indicators are all pointing to a slowdown, which is expected by the end of this year – beginning of the next, at the latest. High interest rates and tightening financial conditions are feeding into the economy, slowly but surely. Some of these effects are already visible in the housing market, with mortgage applications close to a decade low. With housing starts still elevated, it is only a matter of time before prices begin to contract. At the same time, bank credit is falling, especially from smaller regional banks following the financial debacle that took down Silicon Valley Bank (SVB - an example of what happens when the coke machine does fall over). Core inflation (which excludes food and energy prices) remains stubbornly high, and the Federal Reserve (FED) will not take the risk of letting inflation expectations become entrenched in the consumers’ mindsets. This is the reason why we don’t think the FED will cut rates anticipating an economic slowdown; it simply cannot do it. However, we are aligned with the consensus in thinking that rates will be lower towards year-end, but while the former still believes in a soft-landing, we are more inclined to think that lower rates will be the result of the coke machine having rolled over.

That said, for every half-empty glass, there is a half-full one. The economic slowdown is diminishing the excesses in the labour market, as witnessed by the job quit rate which has peaked towards the end of 2022 and is now reverting towards more normalized levels. This is positive news for the FED, as it opens the possibility of acting in case the economy falls into a recession. Simultaneously, rising wages were able to partially preserve the US consumers’ purchasing power, and while not endless, savings from the pandemic relief programs can still support consumption for at least the first half of this year. All in, as we have often written in the past, the US consumer is what is keeping the US economy afloat. High interest rates will force their way into the economy, but sound family balance sheets will ensure the recession will be mild.

Presently, the big elephant in the room is represented by US regional banks, whose wobbly exposure to the faltering commercial real estate sector could have consequences for both the financial system and the economy. More specifically, a tighter regulation will make credit less accessible, having adverse effects on both small and medium-sized enterprises and the labour market. For now, the FED’s corrective actions prevented the unravelling of the situation. Yet, we cannot exclude that SVB and the likes only represented the first piece of the puzzle. Stay alert.

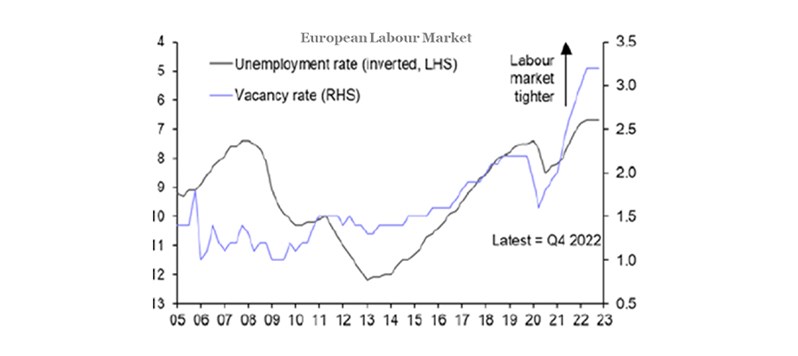

Over to Europe, the milder weather that characterised the beginning of the winter has continued for the remaining of the season, officially declaring the end to an energy crisis that (luckily) never took place. The European economy remains supported by negative real rates but plagued by rising inflation and an excessively tight labour market. We suspect it is only a matter of time until European consumers back down, as rising interest rates will begin to find their way into the former’s consumption habits. Some support will come from the Chinese, who have just emerged from years of widespread lockdowns, through tourism and goods consumption. However, the reopening effect is already losing steam, as recent leading indicators have shown, while domestic consumption remains anchored due to the drags from a moribund real estate sector. We expect monetary authorities to remain vigilant, yet the need to avoid those economic excesses that have characterised the Chinese economy over the past decade will limit both monetary and fiscal stimuli.

FIXED INCOME: PLAY IT SAFE

Given our cautious economic outlook, and despite the fall of interest rates year-to-date (when rates fall, bond prices rise), we still find fixed income investments attractive, and we favour the safer portion of the asset class compared to higher yielding bonds. Naturally, we believe investors should hold long-term government bonds, as they represent the sort of cushion that helps stabilize the performance of any portfolio at times of heightened risks.

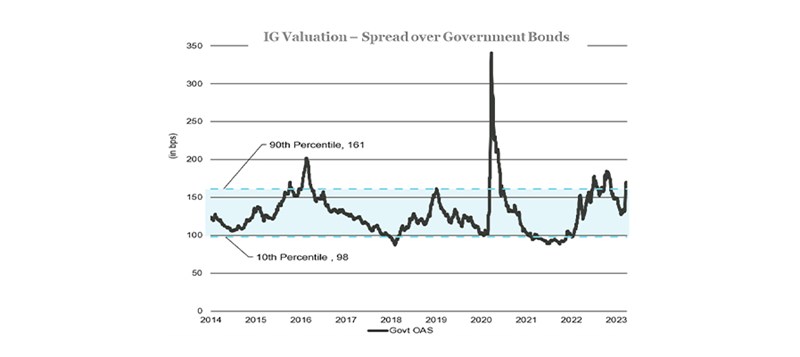

Additionally, as the fundamentals of investment grade issuers remain very solid, even following the surge in interest rates experienced over the past year, we find them attractive, both on an absolute basis and on a relative one. In absolute terms, the current spread against government bonds is trading in the highest decile, while compared to lower-credit issuers, investment grade bonds offer better returns if adjusted for the underlying risk; the fundamentals of high yield companies are deteriorating, and the tightening of lending standards has often acted as a harbinger for further advances in the default rates. On top, the valuation of the segment is also unattractive, as the spread is currently below the long-term average.

At this stage of the economic cycle, and with different bouts of uncertainty cuddling the environment, we suggest avoiding the riskier segments of the asset class and take advantage of the conservative characteristics of both government and investment grade bonds to stabilize the portfolio returns.

If you don’t believe changes in the level of interest rates can affect the economic outlook, then you should pour into equity investments.

EQUITY: OPTIMISM SPREADING, COMPLACENCY RISING

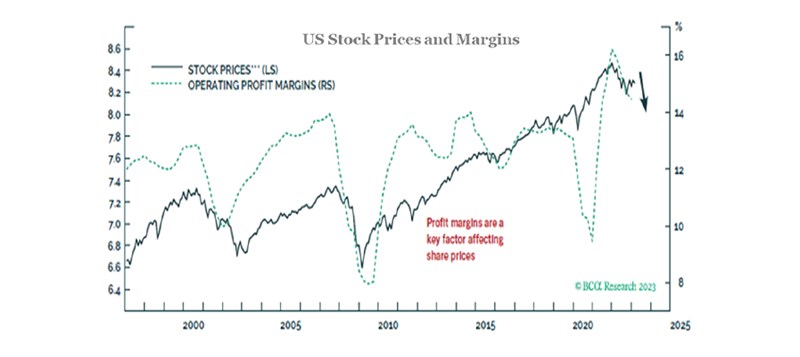

If you don’t believe changes in the level of interest rates can affect the economic outlook, then you should pour into equity investments. On the other hand, if interest rates still matter, then at current valuations equities do not represent an attractive opportunity. In the United States, the last reporting season saw earnings contract, even more so if we exclude the contribution of energy companies, who enjoyed a fantastic year. The current earnings season just started, but with only about ten percent of the companies in the S&P 500 having reported, the statistical relevance is very minimal. More importantly, corporate margins are just off their cycle peak, and their tendency to mean-revert, together with the downward pressure from higher costs and the inability of the final consumer to further absorb rising prices, will constraint profits growth in the future. Simultaneously, equity valuations don’t seem to be offering much of a buying opportunity, as the former are still above long-term averages, despite the correction witnessed during 2022.

In Europe, we observe a similar situation; while Q4 earnings were strong (admittedly, financials and the energy sector did much of the work), the trend is pointing south. The stimuli to fight an energy crisis that luckily never materialized are fading, and the final consumer is subject to rising interest rates. Despite this backdrop, earnings estimates are still up 10% for 2024, which seem unrealistic at this juncture of the economic cycle. On the other hand, European valuations represent a life-vest; they are cheaper compared to US valuations, although this is structural given the lower growth profile of European companies, but they are cheaper also relative to their own history, making us believe that in case of a market correction, European stocks will fare better. The same is true for the Swiss Market Index, whereby investors can gain exposure to resilient businesses that are attractively valued, offering strong visibility on future cash flows and earnings, and thus equipped to better navigate an economic slowdown.

To conclude, we think equity investors are being too complacent with the current economic backdrop; on average, earnings estimates seem too optimistic while equities are fairly valued at best, especially if contextualized in an environment of high inflation, high interest rates, and cracks emerging in the economy.

COMMODITIES AND CURRENCIES: AVOID CYCLICALITY

For both commodities and currencies, it is important to split the analysis between the short-term and the long-term. The green revolution is likely to act as an incubator for commodity prices, as the demand for rare earth, industrial metals, and energy will be on the rise. Meanwhile, as capital expenditure has been dismal over the past decade, supply will not keep up with demand, exacerbating the upward pressure on prices. However, over the shorter-term, with a global economic slowdown around the corner, we would be more selective when it comes to picking commodities. We favour crude oil as a geopolitical hedge and gold in view of lower real rates, but we shy away from more cyclical commodities.

Currency wise, should we be faced with rising volatility across risky assets, the USD would emerge as a clear winner, followed by the CHF. The same is true should inflation resurface, as interest rates differentials would begin to play again in favour of the greenback. On the other hand, focusing purely on fundamentals, we continue to except both the CHF and the USD to depreciate. But fundamentals can take years to play out.

About the author

LFG+ZEST SA